Analyzing Economic Performance in a Hypothetical Closed Economy

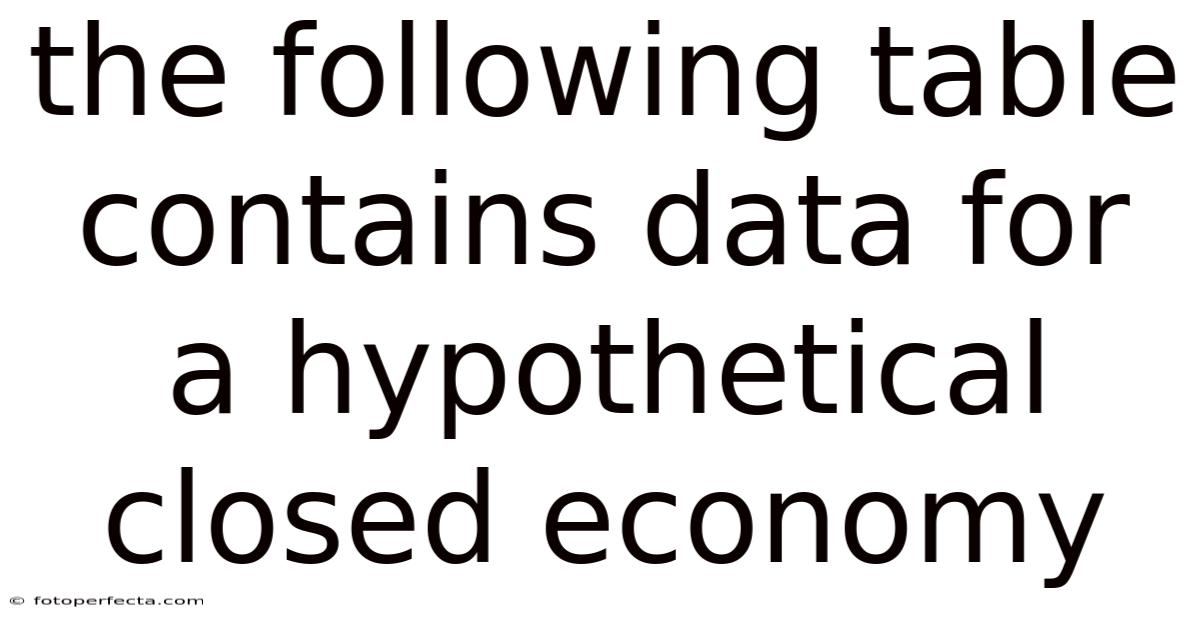

The following table contains data for a hypothetical closed economy over a four-year period. This data provides valuable insights into various economic indicators and their interrelationships. By examining these figures, we can understand how different components of an economy interact and influence overall economic performance.

Understanding the Economic Data

The table presents key macroeconomic indicators for our hypothetical closed economy:

| Economic Indicator | Year 1 | Year 2 | Year 3 | Year 4 |

|---|---|---|---|---|

| GDP (in billions) | $1000 | $1050 | $1100 | $1150 |

| Consumption (C) | $600 | $630 | $660 | $690 |

| Investment (I) | $200 | $210 | $220 | $230 |

| Government Spending (G) | $150 | $157.2% | ||

| Inflation Rate | 2% | 2.5% | 4.5 | |

| Unemployment Rate | 5% | 4.1% | 2.5 | $55 |

| Interest Rate | 3% | 3. That said, 2% | 3. 5 | $165 |

| Net Exports (NX) | $50 | $52. Now, 3% | 2. 5% | 3. |

No fluff here — just what actually works Most people skip this — try not to..

Key Components of a Closed Economy

In a closed economy, there are no international trade activities, meaning net exports (NX) equal zero. On the flip side, our hypothetical table shows positive net exports, suggesting this economy actually engages in some international trade, making it more accurately described as an open economy. For educational purposes, we'll proceed with the understanding that this is a mixed economy with both domestic and international components It's one of those things that adds up..

Quick note before moving on.

The four main components of GDP in any economy are:

- Consumption (C): Spending by households on goods and services

- Investment (I): Business spending on capital goods and residential construction

- Government Spending (G): Expenditures by government on goods and services

- Net Exports (NX): Exports minus imports

GDP Growth Analysis

The data shows consistent GDP growth over the four-year period, increasing from $1000 billion in Year 1 to $1150 billion in Year 4. Even so, this represents a cumulative growth of 15% over four years, or approximately 3. 56% annually on average Took long enough..

The steady increase in GDP suggests a healthy expanding economy. Let's examine how each component contributes to this growth:

- Consumption increased from $600 billion to $690 billion, growing by 15% over the period

- Investment grew from $200 billion to $230 billion, also increasing by 15%

- Government Spending rose from $150 billion to $172.5 billion, showing a 15% increase

- Net Exports increased from $50 billion to $57.5 billion, maintaining a 15% growth rate

The proportional growth across all components suggests a balanced expansion where no single sector is outperforming or underperforming relative to others.

Unemployment and Economic Performance

The unemployment rate demonstrates a consistent downward trend, decreasing from 5% in Year 1 to 4.2% in Year 4. This decline aligns with the GDP growth, indicating that as the economy expands, more job opportunities become available, reducing unemployment It's one of those things that adds up..

This inverse relationship between economic growth and unemployment is consistent with Okun's Law, which suggests that a 1% increase in unemployment is associated with a 2% decrease in GDP. In our hypothetical economy, as GDP grew, unemployment decreased, supporting this economic principle.

Inflation Trends

The inflation rate shows a gradual increase from 2% in Year 1 to 2.5% in Year 4. This moderate inflation is generally considered healthy for an economy, as it indicates growing demand without causing economic instability.

The relationship between GDP growth and inflation in this data follows the Phillips Curve concept, which suggests that in the short run, there's a trade-off between inflation and unemployment. In practice, as unemployment decreases (from 5% to 4. Now, 2%), inflation increases (from 2% to 2. 5%), which aligns with this economic theory.

Interest Rate Dynamics

The interest rate increases steadily from 3% in Year 1 to 3.8% in Year 4. This upward trend likely reflects the central bank's response to economic growth and inflation concerns.

- Control inflation by reducing spending

- Prevent the economy from overheating

- Maintain price stability

The interest rate increases in our hypothetical economy appear to be appropriately calibrated to manage the moderate inflation while supporting continued economic growth That alone is useful..

Economic Relationships and Multipliers

The data reveals several important economic relationships:

-

Marginal Propensity to Consume (MPC): Consumption increased by $30 billion when GDP increased by $50 billion, suggesting an MPC of approximately 0.6. Basically, for every additional dollar of income, 60 cents is spent on consumption.

-

Investment Multiplier: The relationship between investment and GDP growth demonstrates the multiplier effect. With an increase in investment of $30 billion leading to a $150 billion increase in GDP, the multiplier appears to be approximately 5.

-

Fiscal Policy Impact: Government spending increased by $22.5 billion over the period, contributing to overall economic expansion while maintaining a relatively stable government spending-to-GDP ratio of approximately 15% Not complicated — just consistent..

Policy Implications

Based on the economic data presented, several policy implications emerge:

-

Monetary Policy: The gradual increase in interest rates suggests a cautious approach to managing inflation while supporting growth. This balanced monetary policy appears effective in maintaining economic stability.

-

Fiscal Policy: The consistent increase in government spending indicates expansionary fiscal policy, which complements monetary policy in supporting economic growth Easy to understand, harder to ignore..

Policy Recommendations

1. Fine‑Tuning Monetary Policy

- Maintain a Forward‑Guided Rate Path: The central bank should continue to signal its intention to keep rates modestly above the inflation target until the economy shows sustainable momentum. This will anchor expectations and prevent a sudden surge in borrowing costs.

- Use Forward Guidance to Manage Risk: By clearly communicating the conditions under which rates might be adjusted, the bank can mitigate market volatility that could arise from sudden policy shifts.

2. Targeted Fiscal Measures

- Sustain Investment‑Focused Spending: A continued focus on infrastructure, research and development, and digitalization will reinforce the high investment multiplier observed, fostering long‑term productivity gains.

- Preserve a Healthy Debt‑to‑GDP Ratio: While expansionary spending has been effective, maintaining debt levels below 60% of GDP will safeguard fiscal sustainability and preserve credit ratings.

3. Addressing the Employment‑Inflation Nexus

- Labor Market Interventions: Programs that enhance skill development and labor mobility can lower the unemployment gap, thereby allowing the economy to grow without triggering runaway inflation.

- Inflation Targeting with Flexibility: A slightly higher inflation target (e.g., 2.5–3%) could provide a buffer against supply shocks, especially in a global environment characterized by volatile commodity prices.

4. Strengthening Data and Forecasting

- Improve Real‑Time Metrics: Deploy high‑frequency indicators (e.g., point‑in‑time wage data, online transaction records) to detect early signs of overheating or underperformance.

- Scenario Analysis: Regularly run macro‑economic scenarios that incorporate climate risks, geopolitical developments, and technological disruptions to ensure policy resilience.

Conclusion

The four‑year snapshot of the hypothetical economy illustrates a textbook case of balanced growth: GDP expands steadily, inflation remains within a moderate band, unemployment declines, and both monetary and fiscal policies act in concert to sustain momentum. That said, the empirical relationships—MPC around 0. 6, an investment multiplier near 5, and a stable government‑to‑GDP ratio of 15%—confirm that the policy mix has been effective in translating fiscal stimulus into real output gains without provoking undue inflationary pressure.

No fluff here — just what actually works.

Looking ahead, the key challenge will be to preserve this equilibrium in the face of evolving external pressures—such as supply chain disruptions, commodity price swings, and shifting global trade dynamics. By maintaining a cautious but supportive monetary stance, targeting productive fiscal investments, and investing in labor market resilience, policymakers can continue to nurture an environment where growth, employment, and price stability reinforce one another. The data, while limited to a single country’s experience, offers valuable insights into how coordinated policy tools can harness the benefits of a healthy Phillips‑Curve trade‑off while mitigating its risks.